Law of Supply and Demand

The law of supply and demand explains how changes in a product’s market price relate to its supply and demand.

Demand:

Demand is the desire for good/service supported by:

- Willingness (चाहाना )

- Affordability (क्षमता)

Example: a person when young doesn’t think a bike is safe. So he doesn’t have a willingness to buy bike although he can afford it creating no demand. He wants a car but it is not affordable. So, no demand is created even he has the desire. So, in order to create a demand both desire and affordability is required.

| Willingness | Affordability | Demand | |

| Bike | X | ✓ | X |

| Car | ✓ | X | X |

- To increase demand either increase willingness (one method advertisement)

or increase affordability ⟹ reduce price Eg: car in installment, etc.

Law of Demand:

“When all else is equal, as the price of a good rises, the quantity demanded by consumers falls. Conversely, when the price falls, quantity demanded increases.”

Demand(D)= f( price, p)

:max_bytes(150000):strip_icc():format(webp)/law_of_demand_chart2-5a33e7fc7c394604977f540064b8e404.png)

So there is an inverse relation between price and demand. This inverse relationship is due to two main effects:

- Substitution Effect: Consumers shift from relatively more expensive goods to cheaper ones.

- Income Effect: A lower price increases consumers’ purchasing power, enabling them to buy more.

Demand Curve: A demand curve illustrates the number of units people are willing to buy at different price points, and it typically slopes downward.

Inverse Law of Demand: If demand increase price increases and vice-versa. P=f(D) (price as a function of demand)

There are many cases when the law of demand might seem to be violated. Eg: If consumers associate a higher price with higher quality, they might demand more of the product even as the price increases like people buy i-phones (high demand) even though it is very expensive relative to it’s competitors. Some more examples:

- Necessities: Demand for salt, rice remains stable even if the price rises.

- Luxury goods: Expensive designer handbags may see higher demand when prices rise, as they signal exclusivity.

- Consumer preference: A trendy smartphone may stay in high demand despite price hikes (i-phones).

- External factors: If people’s income rises, they may buy more organic food, even at higher prices.

- Perceived quality: A higher-priced perfume may sell more because buyers assume it’s premium quality.

- Future expectations: If fuel prices are expected to rise, people may rush to fill their tanks now.

- Market manipulation: Limited-edition sneakers (सामान लुकाएर राख्ने) often have high demand at inflated prices due to artificial scarcity (like LPG and petrol scarcity that were created in Nepal at times).

Factors Affecting Demand:

- Price: inverse relation: lower price → higher demand – law of demand itself

- Income: higher income → higher demand → demand curve shifts to right and vice-versa

- Related goods: price change in one affects demand for another

- Consumer tastes: preferences shift demand. eg: more incidence of diabetes → increase in insulin demand

- Elasticity: necessities have stable demand (eg: rice, salt), luxuries are price-sensitive (eg: mutton, chicken)

Supply:

Supply in economics refers to the amount of a good or service that producers are willing and able to offer for sale at various prices during a given period, holding other factors constant.

Law of Supply:

- “Keeping other factors constant, as the price of a good increases, the quantity supplied by producers also increases; when the price falls, the quantity supplied decreases.”

- Supply = f (Price)

- This direct relationship is based on profit motives: higher prices make it more profitable to produce additional units.

:max_bytes(150000):strip_icc():format(webp)/Supplyrelationship-c0f71135bc884f4b8e5d063eed128b52.png)

Factors Affecting Supply:

- Price of the product: Lower prices discourage production, reducing supply (law of supply itself).

- Cost of inputs: Higher costs reduce supply (e.g., expensive raw materials limit production).

- Technology: Better technology lowers costs, increasing supply (e.g., automation in factories).

- Weather: Seasonal changes impact supply (e.g., more woolen products in winter).

- Prices of related goods: Demand shifts in related products influence supply (e.g., cheaper TVs boost VCD supply).

Supply Curve:

- Graphical Orientation: Price on the y-axis, quantity on the x-axis.

- Upward Sloping: Higher prices encourage more production.

- Ceteris Paribus (All Else Equal): The supply curve assumes factors like technology and input costs stay constant—only price changes affect movement.

- Marginal Costs: Rising output increases marginal costs, requiring higher prices. As production increases, costs rise, so higher prices are needed to motivate production (e.g., hiring more workers increases costs).

- Elasticity: Short-run supply is inelastic; long-run supply is more flexible. Short-term supply is harder to change (e.g., factories can’t instantly increase car production), but long-term adjustments make supply more flexible.

- Movement vs. Shift: Price changes move along the curve; other factors shift it.

Elasticity of Demand and Supply:

Price Elasticity of Demand (PED):

- This measures how demanded changes with changes in price.

- Formula:

Example:

| Rice Qty | Price | Chicken Qty | Price |

| 25 kg rice | Rs. 1500 | 2 kg | Rs. 250 |

| 24 kg | Rs. 2500 | 0.5 kg | Rs. 500 |

So rice is less elastic w.r.t chicken in terms of demand. Even though the price of rice changed significantly the demand for rice didn’t as much as compared to that of the chicken. (Necessity vs Luxury Item)

Price Elasticity of Supply (PES):

- Similarly, PES measures how supply changes with change in price.

- Formula:

- Eg: Here’s a brief comparison in table form:

| Good | Price Increase | Quantity Supplied Increase | Elasticity (Eₛ) | Reason |

|---|---|---|---|---|

| Oranges 🍊 | 20% | 5% | 0.25 | Takes time to grow, cannot increase supply quickly. |

| T-Shirts 👕 | 20% | 50% | 2.5 | Can be produced quickly with more labor/machines. |

So, T-shirts are more elastic in terms of supply as compared to oranges.

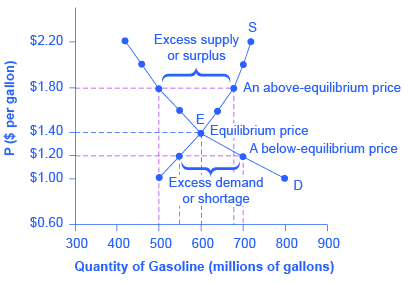

- The intersection of the supply and demand curves is known as the equilibrium point.

- At the price corresponding to the equilibrium point, the quantity of supply is equal to the quantity of demand.